In a New Jersey workers’ compensation case, “permanency” refers to the final phase of a claim where an injured worker is evaluated for a financial monetary award due to a lasting, permanent loss of...

When litigating personal injury and employment-related torts in New Jersey, defendants frequently move for summary judgment on direct negligence claims, such as negligent hiring or negligent...

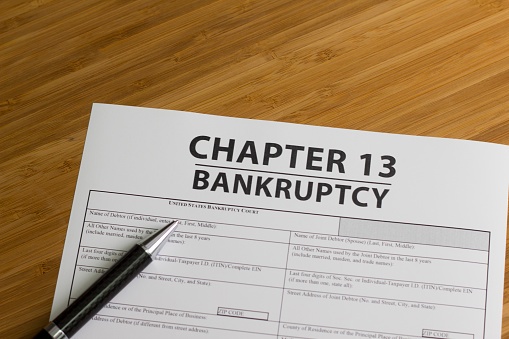

Voluntarily dismissing your Chapter 13 bankruptcy does not necessarily end the bankruptcy court's authority. Here's what debtors and creditors need to know.

When a Chapter 13 repayment plan is confirmed, many debtors understandably believe their case is settled. Likewise, creditors often assume the confirmation order is the final word. In most...

When a Chapter 11 bankruptcy estate has enough assets to pay every creditor in full—and still has money left over, how is the Chapter 11 trustee compensated? The answer is more nuanced than many...

The shift toward remote and hybrid arrangements has fundamentally rewritten the rules between New Jersey employers and their staff. For HR professionals and in-house counsel, this reality brings a...

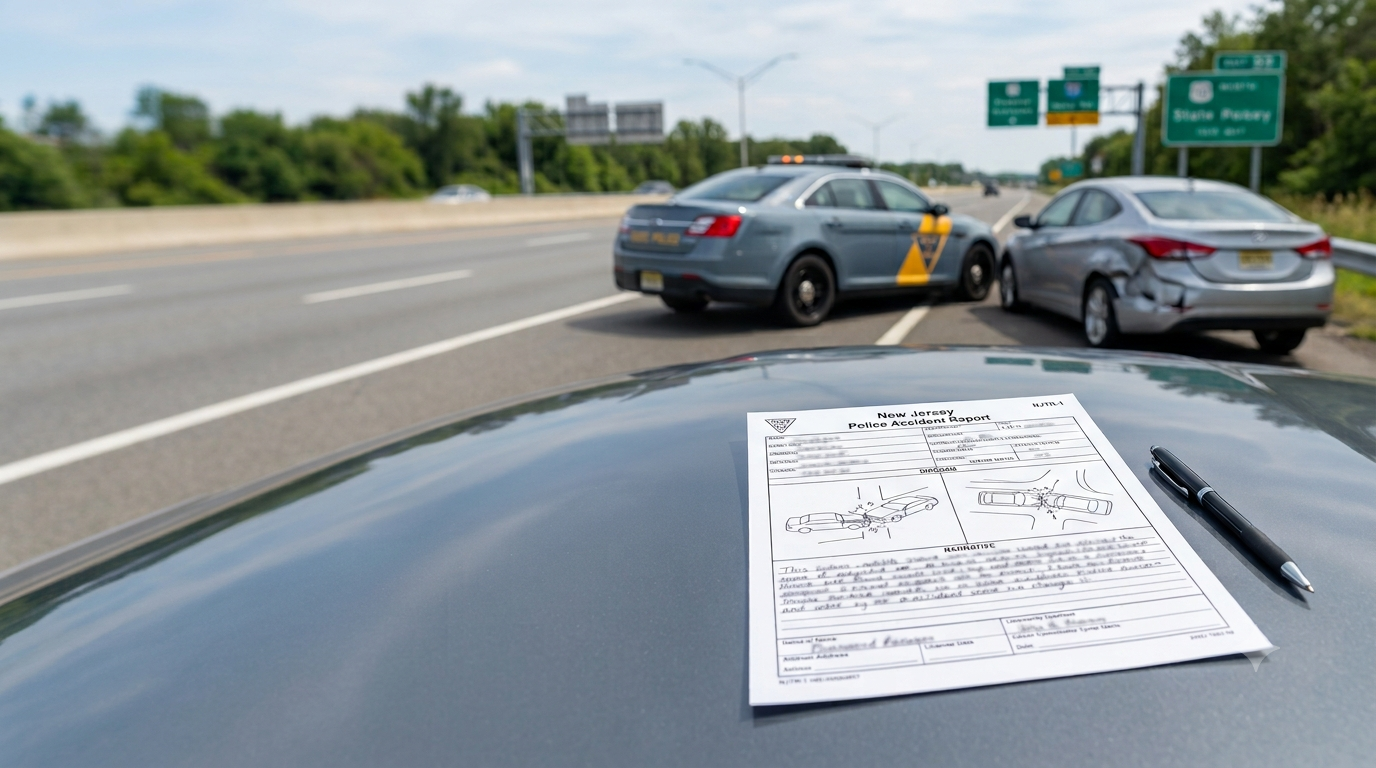

E-bikes have become increasingly common throughout New Jersey. They are used for commuting, deliveries, recreation, transportation around shore towns, and getting around congested cities where...

Imagine you are seriously injured in a car accident through no fault of your own. You do everything right: you maintain insurance, seek medical treatment, and pursue a claim against the at-fault...